May 2026 Survey: The Recovery is on Track Despite Risks

At the start of the year, the cyclical outlook looked promising. Finland finally posted modest growth at the end of last year, and many expected the momentum to carry into 2026. On the export side, the recovery was set to benefit from a calmer U.S. tariff stance and expansive fiscal policy in Europe. On the domestic side, improving purchasing power was expected to lift private consumption. With trade policy stabilizing, the global economy also appeared resilient.

However, so far, the year 2026 has been anything but calm. The brief disputes involving Venezuela and Greenland faded quickly, but the war in Iran has proven to be much more consequential. Even so, while the conflict with Iran and the resulting surge in energy prices have weakened the outlook, the recent Finland chamber of commerce business survey in April does not support the pessimistic interpretation that the domestic recovery would have been derailed.

Results were slightly weaker than in the January survey, but they remained solid. Although respondents described overall sentiment as pessimistic, expectations for future revenue, order books and exports remained positive. Given the substantial rise in uncertainty, only a limited weakening can be regarded as good news.

Downside risks are evident. If the Strait of Hormuz remains closed for an extended period, the economic impact intensifies. In a worst-case scenario, oil prices could rise sharply from already elevated levels, with price pressures spreading beyond energy to a broad range of raw materials. That would accelerate inflation, squeeze households’ purchasing power and force central banks to tighten monetary policy. A rise in interest rates could push Finland back into recession. However, the baseline assumption is that the most acute phase will be temporary and economic damage limited.

Uncertainty and higher energy prices are dampening growth, but supportive factors remain. Households’ purchasing power has already recovered considerably and should continue to improve, albeit more slowly than previously estimated. Despite the uncertainty, also the export outlook remains reasonably favourable.

Expectations for revenue over the next six months remain positive. About 36% of respondents anticipated an increase, while clearly fewer—around 19%—expected a decline. In January, the corresponding shares were 37% and 15.7%. In other words, expectations are broadly unchanged, although the share anticipating a fall has risen somewhat. The remainder expected revenue to be stable.

More than 80% of respondents still expect revenue to be at least unchanged, suggesting no broad-based deterioration in sentiment. Expectations are particularly strong among larger enterprises, which carry significant weight for GDP.

The current assessment of order books is not yet great, and the situation has not changed materially since the start of the year. In the latest survey, 29.5% of respondents for whom order books are relevant assessed them as stronger than a year earlier, while 32.6% reported weaker order books. For the remainder, the situation was unchanged.

By sector, construction had the weakest order-book situation, as expected. Manufacturing, in contrast, showed clear improvement: 39% of respondents said their order books were stronger than a year earlier, while 24.4% reported weaker order books.

Expectations for the development of order books remained supportive. Over the next six months, 31.2% of respondents expected improvement, 18.8% expected deterioration, and 50% expected no change. Overall, the results point to a continuing recovery, though with less momentum than was expected at the start of the year.

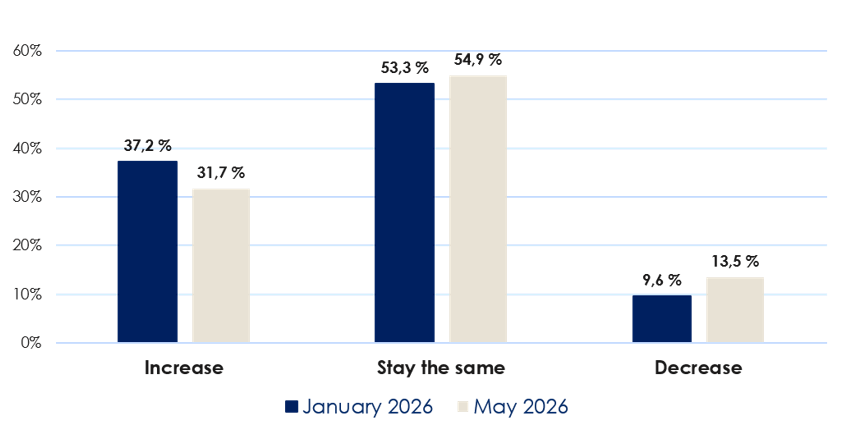

A similar pattern is visible in export expectations. Compared with January, expectations weakened somewhat, but they can still be described as robust. Just under 32% of exporters expected growth this year, while 13.5% anticipated a decline (January: 37.2% and 9.6%). Given the softening global outlook and higher uncertainty, the latest results are still encouraging. This is notable because goods exports held up reasonably well already in 2025 despite an otherwise sluggish domestic economy, so the comparison base is not especially low.

Raw material costs have increased sharply, and further increases cannot be ruled out. It is therefore unsurprising that profitability expectations weakened. Many enterprises find it difficult to pass higher costs through to prices, which puts pressure on margins.

Even so, the overall picture is not particularly alarming. Some 29.7% of respondents expected profitability to improve over the next six months, while 31.5% expected it to weaken. The balance remains close to even, but the share anticipating deterioration has risen (January: under 22%).

Respondents continued to describe sentiment in their industries as very pessimistic. Sentiment measures in surveys have been bleak for a prolonged period, largely reflecting a long-lasting weak business cycle. In April, only 18.6% of respondents described their industry mood as optimistic or very optimistic (January: 20.9%). The share calling it pessimistic or very pessimistic rose from 42.6% to nearly 46%. Importantly, these assessments of broad industry-level sentiments do not align with the relatively positive expectations many respondents report for their own activity. Ultimately, enterprise-level performance matters, not sentiments.

Will Growth Continue?

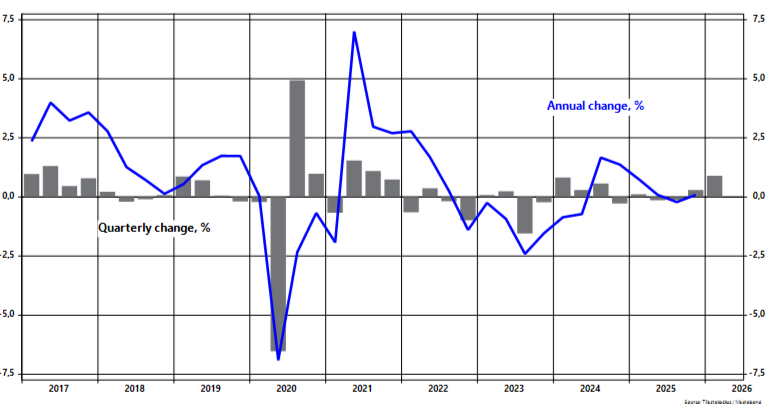

Overall, 2025 was a weak year, and economic growth fell far short of expectations. Current estimates suggest that GDP rose by just 0.2% over the year, well below the typical approximately 1.5% growth forecasts made at the start of the year. Even so, the year ended on a more positive note. In the final quarter GDP turned to a cautious—yet encouraging—0.3% quarterly increase. According to preliminary estimates, the growth has continued and accelerated in the beginning of 2026.

Finnish GDP

Despite encouraging preliminary growth figures, companies’ already downbeat assessments of sentiment in their industries weakened further in the latest chamber of commerce survey. Sentiment indicators began to weaken in 2022 after Russia’s invasion of Ukraine. Pessimism reached its low point in autumn 2023, but there has been no significant improvement since, even though readings vary somewhat from one survey to the next. It is worth emphasising that this reflects the general mood in each industry, not the performance of an individual company.

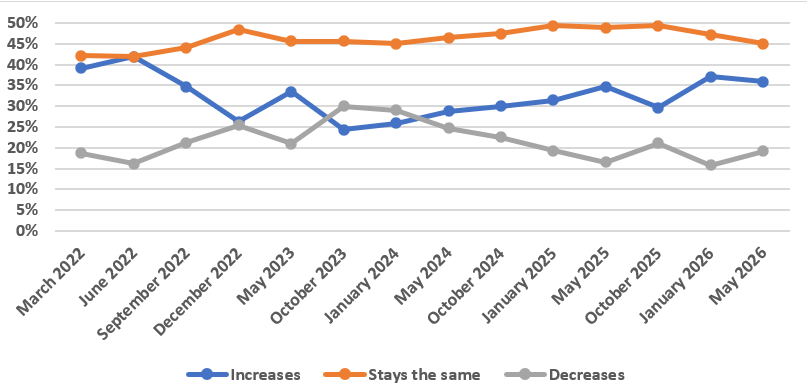

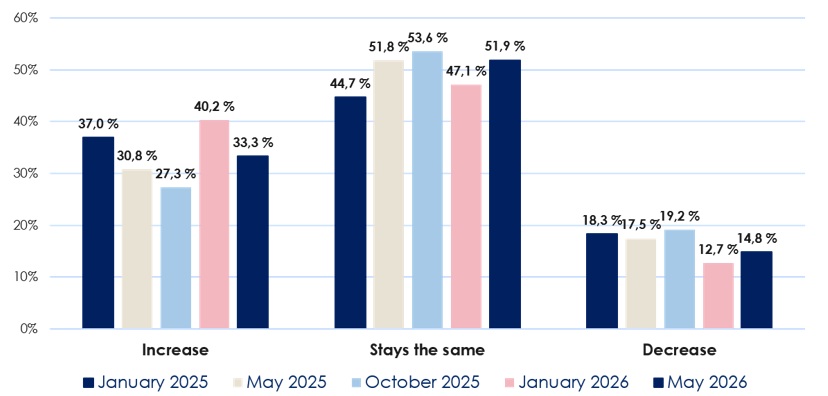

Despite the gloomy overall mood, companies’ expectations for their own revenue over the next six months are clearly more upbeat. In the latest survey, about 36% of respondents expected revenue to grow over the next six months. The corresponding figure in January was 37%, so sales expectations have not deteriorated materially. In April, 19.1% expected revenue to decline—somewhat higher than the 15.7% recorded in January.

Even so, the share of respondents expecting weaker revenue remains small, which keeps the overall picture supportive. One interpretation is that most firms do not expect global turbulence to materially affect their business, while a smaller group anticipates clearer spillovers. In both surveys, the largest group expected revenue to remain unchanged.

Expectations for Revenue Growth Over the Next 6 Months

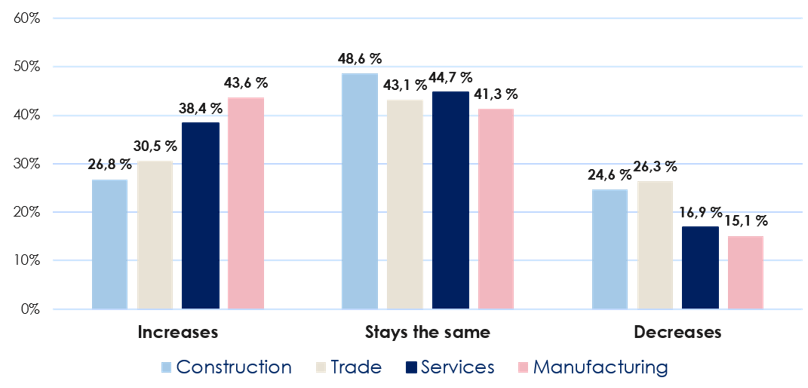

Revenue growth expectations were weakest in construction, though even there slightly more respondents expected growth than decline. Somewhat surprisingly, expectations weakened in trade rather than manufacturing, despite manufacturing’s greater exposure to global uncertainty and interest rates. In fact, manufacturing revenue expectations have improved and are now very strong. In trade, by contrast, respondents appear doubtful that domestic demand will strengthen and remain concerned about price pressures and households’ ability to absorb higher prices given weak consumer confidence.

Expectations for Revenue Growth Over the Next 6 Months

Weak demand remains by far the main constraint on output. The situation improved slightly from January: 53.3% of respondents still cited insufficient demand, but this was the second consecutive survey to show easing demand pressures. In October, the figure was 59.7%, a decline large enough to be unlikely to reflect survey noise alone. Even so, conditions remain difficult. In the first chamber of commerce cyclical survey in March 2022, the corresponding figure was still below 17%.

By contrast, a growing share of respondents cites heightened geopolitical tensions as a constraint on operations, which is understandable. In the latest survey, 43.3% emphasized geopolitics, up from 28% in January. Uncertainty complicates long-term planning and investment decisions, and—as expected—geopolitical risks are most pronounced in manufacturing and among larger companies.

On trade policy front, the situation is currently clearly calmer than during last spring. It could change given Trump’s unpredictability, but it may be less likely that he would add further disruption—and domestic inflationary pressure—ahead of the November midterm elections, especially after the Iran conflict has weighed on president’s popularity.

In stronger cyclical phases, shortages of skilled labour have often become a major brake on Finland’s economy. At present, labour shortages are the exception and mainly reflect matching problems rather than a broad lack of available workers. In the latest survey, only 17% of respondents said labour shortages significantly constrained their operations. The limited shortage reflects both weak labour demand and an unusually strong labour supply relative to the cycle.

Instead, rising raw-material prices—amplified by war-related availability constraints linked to the Iran conflict—have become a much bigger challenge than before. In the latest survey, nearly 30% of respondents cited higher raw-material costs as a constraint, up from just over 11% in January. Price pressures increased in all sectors except services, with the sharpest rises in manufacturing and construction.

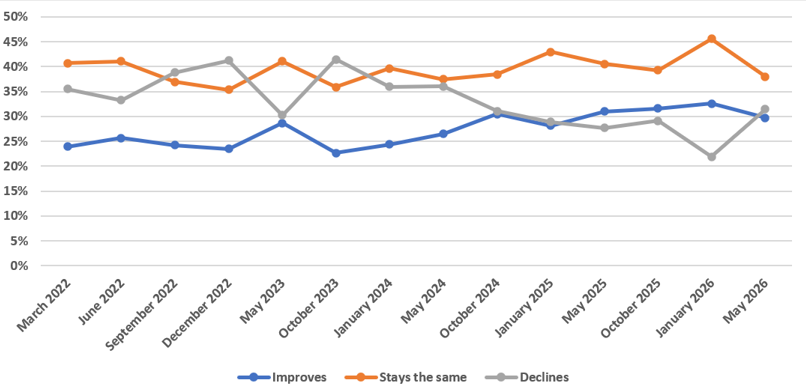

These cost pressures are also reflected in profitability expectations, which weakened compared with the start of the year. In particular, the share expecting profitability to deteriorate increased: whereas in January fewer than 22% anticipated a decline, the figure has now risen to 31.5%, the highest in two years. With the cycle still fragile, many firms struggle to pass higher input costs on through to their selling prices.

By contrast, the share expecting profitability to improve dipped only slightly. Even after the weakening, the figures are still relatively good, although this time slightly more respondents expect deterioration than improvement.

A reasonable reading is that profitability is deteriorating mainly among firms for which the recent cost surge is particularly material. Working in the opposite direction are gradually improving demand conditions and a slowly strengthening cycle. Which force dominates varies from company to company. Profitability expectations weakened across all sectors, most notably in trade and construction.

How do you expect your profitability to develop over the next 6 months?

Export Expectations Have Held Up

Last year was challenging for the global economy as uncertainty and tariff volatility weighed on sentiment. Ultimately, the worst fears did not materialise: the global economy again proved adaptable and international trade expanded towards the end of 2025. In the second half of the year, tariff policy stabilised, and expectations were that 2026 would unfold more steadily, with growth at least around its long-term average.

Much changed at the end of February, when the United States and Israel attacked Iran on a clearly broader scale than anticipated, triggering a conflict that once again threatens global economic stability. The single biggest pressure point is the Strait of Hormuz, which remains mostly closed. Normally, over 20% of the world’s oil and natural gas flows through the strait, along with many other raw materials such as fertilisers and helium used in semiconductor manufacturing. The result has been a massive price shock, especially in energy. The danger is a broader inflation spike and, in the worst case, a subsequent wage–price spiral and a de-anchoring of inflation expectations.

It is clear that the raw-material price shock, accelerating inflation, uncertainty and rising interest rates will all slow global growth—at least this year. Much depends, however, on how long the acute crisis lasts and how long the Strait of Hormuz remains closed. A prolonged crisis would lead to recession, but that is not the main assumption at this stage. The baseline is that both the euro area and the United States will continue to grow, albeit more slowly than previously expected.

The April survey suggests that exporters remain relatively confident. Most continue to expect growth—or at least stable conditions—and do not believe the disruption in the Strait of Hormuz will significantly derail exports.

Compared with last year, exports will

Among exporting respondents, 31.7% expected exports to grow this year, while 13.5% expected a decline. Although expectations weakened compared with the start of the year (37.2% and 9.6%, respectively), the overall picture remains strong. In total, 86.5% of respondents expect exports to be at least at last year’s level, and only a small share anticipates weakening. In manufacturing, firms are also supported by a stronger order-books than before. While new industrial orders are volatile month to month, the underlying order flow has been on an upward trend for some time.

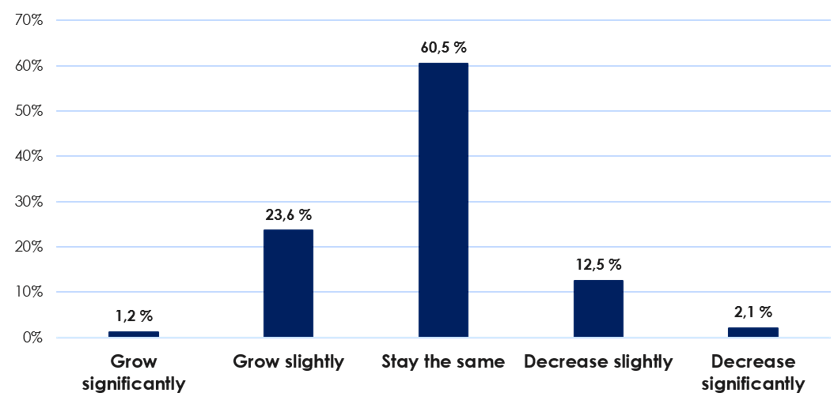

The softer cycle does appear to be showing some strain in expectations for future order books, which have levelled off compared with the start of the year. Even so, the latest readings remain very solid. In manufacturing, 33.3% of respondents still expected their order books to strengthen over the next six months, while only 14.8% expected weakening.

Manufacturing: Expected Order-Book Development Over the Next 6 Months

Consumer Confidence Low, Unemployment High

Already weak consumer confidence has deteriorated following the current crisis in Iran. In April, the indicator stood at -12.5, versus a long-term average of -2.9. The level is close to that seen during the 2007–2008 financial crisis and in spring 2020, when the coronavirus pandemic began. Significantly lower readings have been recorded only in 2022 after Russia’s invasion of Ukraine and possibly during the early-1990s depression, though the current time series does not extend that far back.

Households were downbeat across all components of the confidence indicator. Assessments of both current personal finances and the outlook were weak, as were expectations for Finland’s overall economy. Only 14% of respondents believed the macroeconomy would improve over the next year—considerably more pessimistic than professional forecasts.

Consumer confidence is currently weighed down by geopolitical uncertainty and rising unemployment. In the two most recent readings, the Middle East crisis appears to have pushed already weak confidence lower, which is also reflected in higher inflation expectations. Intentions to buy a home were at their lowest level since the 1990s. Fear of unemployment is elevated, even if it remains below the levels observed during the financial crisis or the coronavirus pandemic. These concerns are partly consistent with labour-market developments: the increase in unemployment has been concentrated primarily among younger cohorts and in the ending of fixed-term contracts, while unemployment among prime-age workers in permanent employment has risen less markedly.

Alongside higher interest rates and prices, weak consumer confidence is likely to restrain a recovery driven by domestic consumption. At the same time, it should be noted that, despite higher inflation, households’ purchasing power is likely to increase fairly briskly this year owing to sizeable wage agreements. Only a sharp acceleration in inflation would materially change this assessment, which does not appear likely at present. Inflation is higher than previously forecast, but conditions for a recovery in private consumption remain in place, albeit more muted than previously envisaged.

How will the number of your employees develop over the next 6 months?

In the latest chamber of commerce survey, expectations for employment developments were relatively strong. Of respondents, 24.9% anticipated increase over the next six months, while 14.6% expected a decrease. The shares are broadly unchanged from January.

The survey design is likely to overstate positive employment outcomes, as a sizeable share of job losses arises from bankruptcies or large one-off events whose scale is not well captured by the survey. Nevertheless, compared with earlier surveys, employment expectations have improved. To find stronger expectations for headcount growth, one has to go back around two years. The survey therefore supports the view that labour-market conditions may start to gradually improve gradually in the future.

Picture: Liisa Takala